Learn when Malaysian importers must issue self-billed e-invoices for multiple shipments under a foreign supplier's invoice. Easy guide with examples.

Table of Contents

Self-Billed e-Invoice Rules for Malaysian Importers

For Malaysian importers, managing self-billed e-Invoices can be complex, especially when goods are delivered across multiple shipments under a single invoice from a foreign supplier.

The question many importers ask is:

"When do we need to issue the self-billed e-Invoice, and for which shipments?"

This guide explains the rules surrounding self-billed e-Invoices in a clear and professional manner. By addressing three common scenarios, you will gain a comprehensive understanding of when and how to issue self-billed e-Invoices in compliance with customs and tax regulations.

What is a Self-Billed e-Invoice?

A self-billed e-Invoice is an invoice issued by a Malaysian buyer (importer) on behalf of a foreign supplier for imported goods.

It is a mandatory requirement that importers must issue the self-billed e-Invoice by the end of the month following the month in which customs clearance is obtained. This ensures proper reporting of import transactions and aligns with the Royal Malaysian Customs Department (RMCD) guidelines.

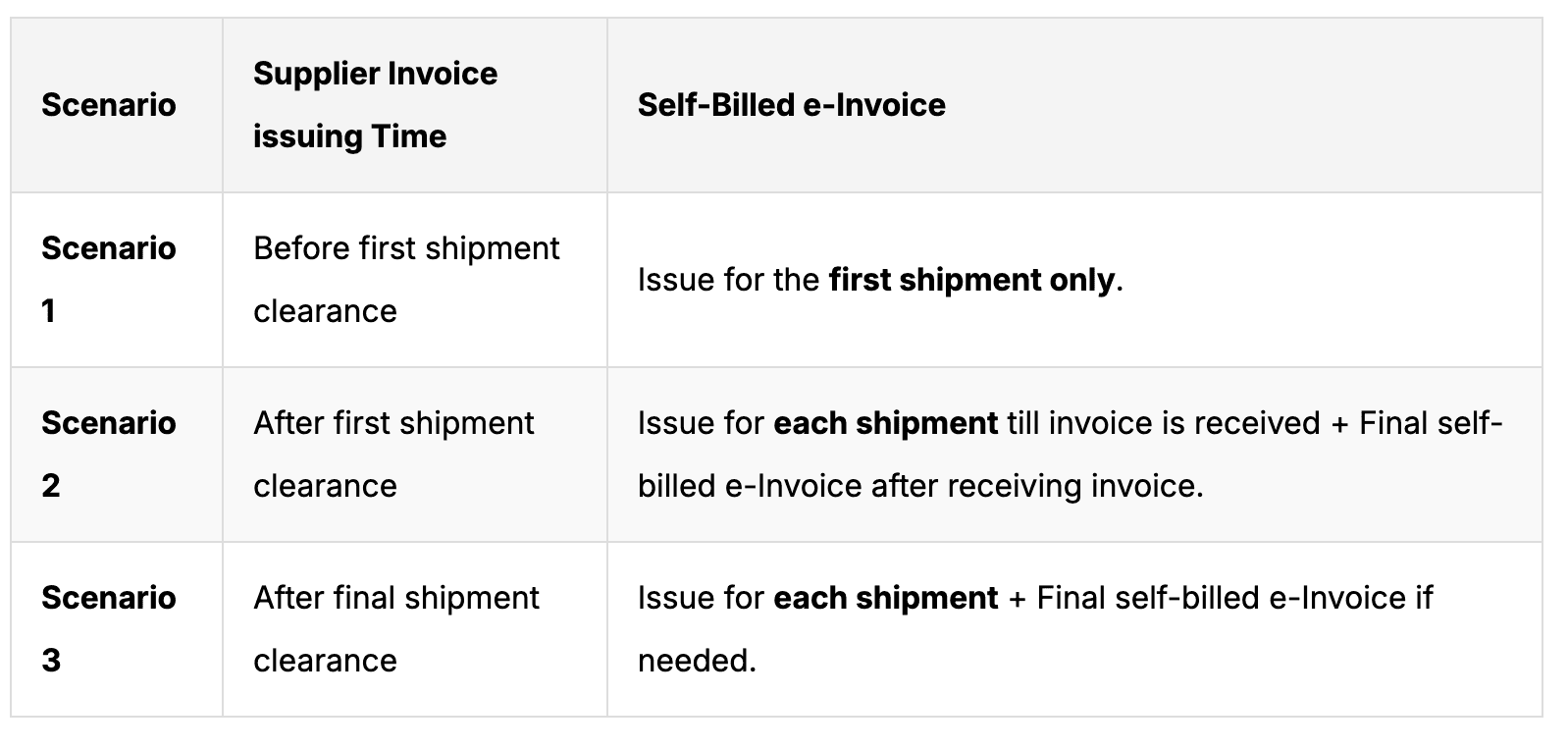

Three Scenarios for Issuing Self-Billed e-Invoices

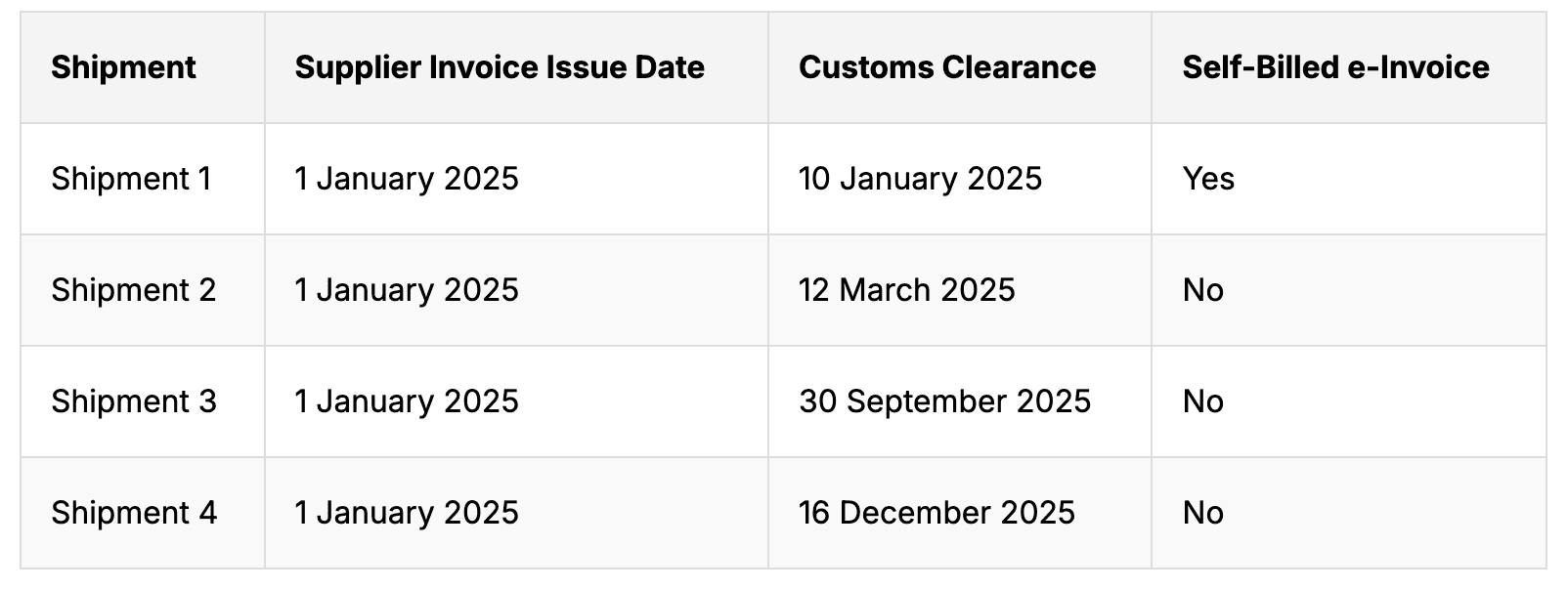

Scenario 1: Supplier’s Invoice Issued Before the First Shipment Clearance

If the foreign supplier issues the invoice before the first shipment clears customs, the Malaysian buyer must:

Issue one self-billed e-Invoice for the first shipment clearance.

No additional self-billed e-Invoices are required for the subsequent shipments under the same invoice.

Example:

Key Takeaway: Only one self-billed e-Invoice is required when the supplier’s invoice is issued before the first shipment clearance.

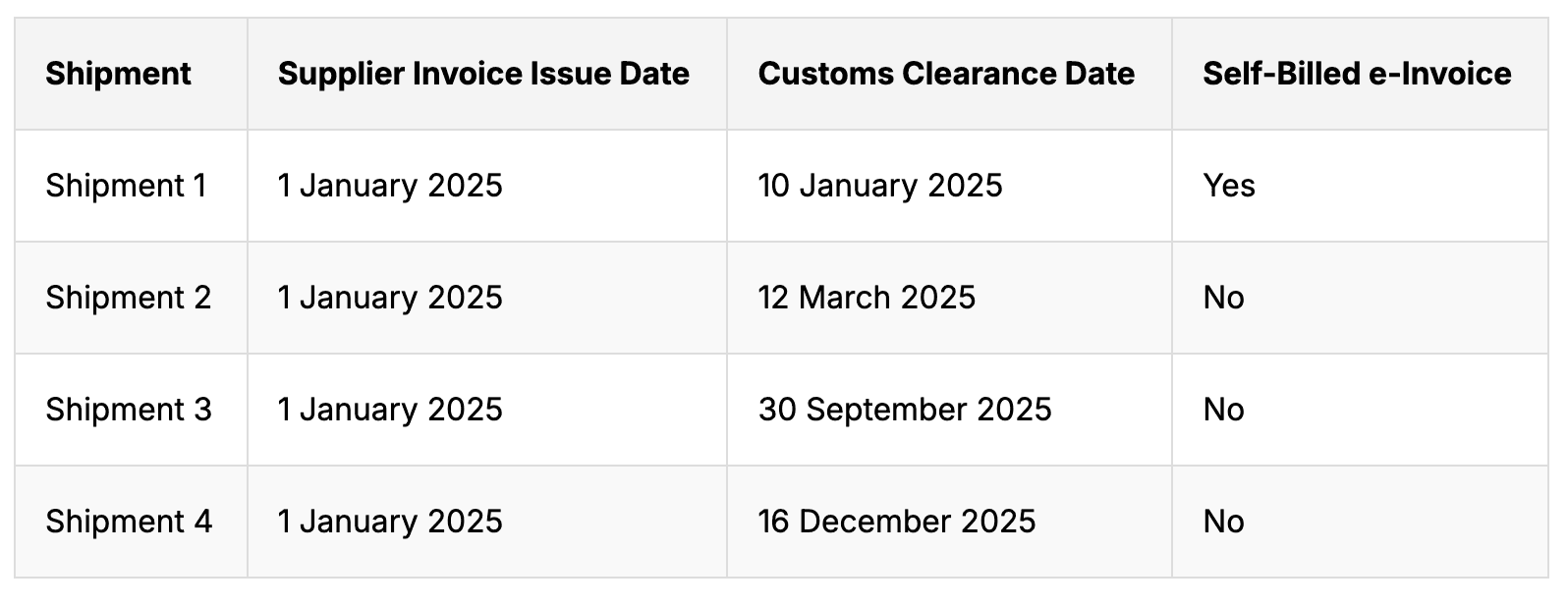

Scenario 2: Supplier’s Invoice Issued After the First Shipment Clearance

If the supplier issues the invoice after the first shipment has cleared customs, the Malaysian buyer must:

Issue a self-billed e-Invoice for each shipment as it clears customs till supplier’s invoice is received.

Once the supplier’s invoice is received, issue a final self-billed e-Invoice to align the amounts declared.

Example:

Final Invoice Issuance:

When the supplier issues the invoice on 1 October 2025, the buyer must issue a final self-billed e-Invoice to reconcile the total amount.

Key Takeaway: Self-billed e-Invoices must be issued for each shipment cleared before the supplier’s invoice is received. A final self-billed e-Invoice ensures consistency with the supplier’s declared amounts.

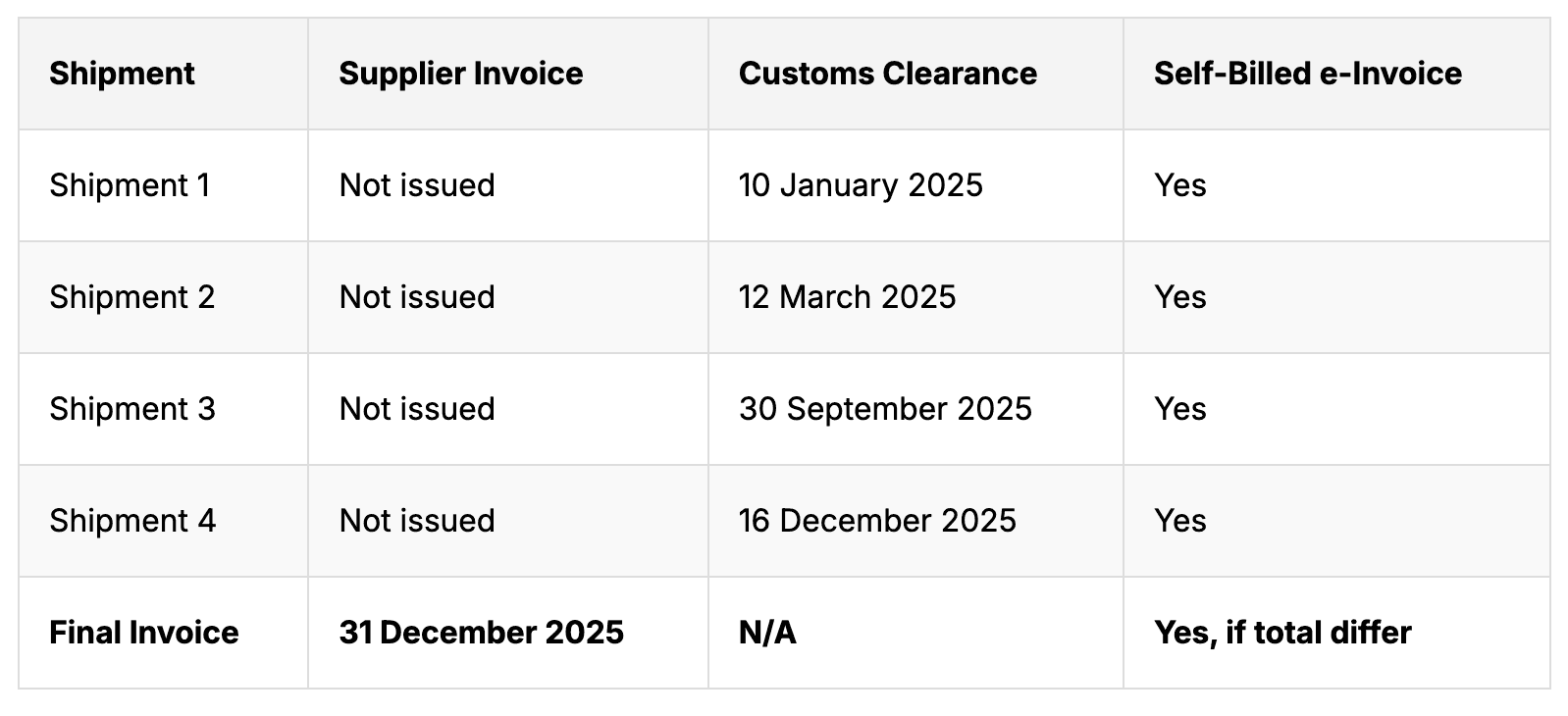

Scenario 3: Supplier’s Invoice Issued After the Final Shipment Clearance

If the supplier issues the invoice only after all shipments have cleared customs, the Malaysian buyer must:

Issue a self-billed e-Invoice for each shipment as it clears customs.

Once the supplier’s invoice is issued, a final self-billed e-Invoice is required if there is a discrepancy in the total declared value; if there is no discrepancy there is no need for a final self-billed e-Invoice.

Example

Key Takeaway: Self-billed e-Invoices must be issued for each shipment cleared. A final self-billed e-Invoice must be issued if the total declared value differs from the supplier’s invoice.

Summary of Scenarios

Complyance Tips for Malaysian Importers

To remain compliant and avoid penalties:

Maintain Accurate Records: Track the supplier invoice date, shipment clearances, and customs forms.

Timely Issuance: Issue self-billed e-Invoices by the end of the month following the month of customs clearance.

Customs References: Include the customs form reference number (e.g., Customs Form No. 1) in all self-billed e-Invoices.

Reconcile Totals: Ensure the total amount declared aligns with the supplier’s final invoice.

Conclusion

For Malaysian importers handling multiple shipments under one foreign supplier invoice, understanding when to issue self-billed e-Invoices is essential.

Whether the supplier’s invoice is issued before, during, or after customs clearances, following the rules ensures compliance with RMCD regulations and smooth business operations.

By issuing self-billed e-Invoices on time and reconciling values accurately, importers can avoid unnecessary delays and penalties.

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.