Learn about Malaysia's e-invoicing regulations for cross-border transactions, requirements, processes, and best practices for compliance.

Table of Contents

Malaysian E-Invoicing Regulations for Cross-Border Transactions

Cross-border transactions refer to trade activities between a Malaysian buyer and a foreign supplier or vice versa. This includes the sale of goods or the provision of services by a foreign seller to a Malaysian purchaser, and the sale of goods or services by a Malaysian seller to a foreign buyer.

Malaysia has implemented specific guidelines for cross-border transactions to ensure adherence to local tax regulations. These guidelines require Malaysian purchasers to issue self-billed e-invoices when dealing with foreign suppliers who are not obligated to use Malaysia’s e-invoicing system.Cross-border transactions occur when there's a trade between a buyer in Malaysia and a supplier from another country, or the other way around.

A foreign supplier is anyone who operates outside of Malaysia, whether they are a business or an individual not based in Malaysia. On the flip side, a foreign buyer is any person from another country who purchases goods or services from Malaysia.

There are two main types of cross-border transactions:

Goods or services provided by a foreign seller to a buyer in Malaysia.

Goods or services provided by a seller in Malaysia to a foreign buyer.

Goods or services provided by a foreign seller to a Malaysian buyer

Currently, when a Foreign Seller conducts a transaction with a Malaysian Purchaser, such as selling goods or providing services, the Foreign Seller will issue an invoice, bill, or receipt to document the transaction.

The invoice, bill, or receipt is created following the local invoicing regulations of the Foreign Seller’s country as part of their standard business practices.

Since the Foreign Seller is not required to comply with Malaysia’s e-Invoice regulations, it falls upon the Malaysian Purchaser to generate a self-billed e-Invoice to record the expense. This self-billed e-Invoice is crucial for tax documentation purposes.

For the self-billed e-Invoice process, the roles are defined as follows:

Supplier: Foreign Seller

Buyer: Malaysian Purchaser (acting as the Supplier to issue the self-billed e-Invoice for expense documentation)

The steps for the Malaysian Purchaser to issue a self-billed e-Invoice are outlined below:

Step 1: Once a transaction is completed, the Foreign Seller will provide an invoice, bill, or receipt to the Malaysian Purchaser, recording the revenue from the sale of goods or services provided.

Step 2: The Malaysian Purchaser must then take on the role of the Supplier and issue a self-billed e-Invoice to document the expense for tax purposes. This must be done according to the required timing.

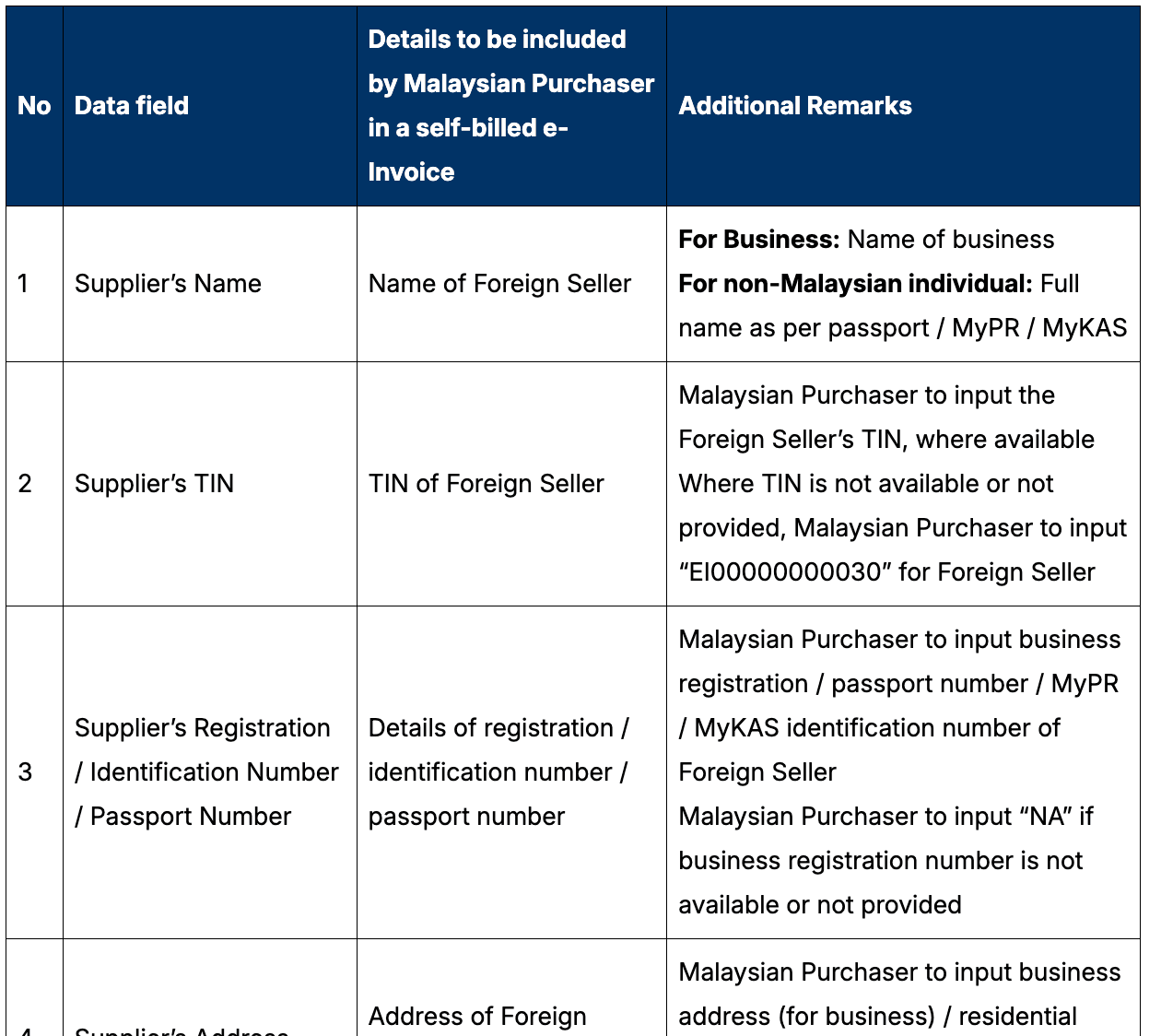

When issuing the self-billed e-Invoice, the Malaysian Purchaser should fill out the necessary fields. The details from the Foreign Seller's invoice, bill, or receipt can be used, or the required information can be requested from the Foreign Seller.

If certain details are unavailable because they do not apply to the Foreign Seller or were not provided, the Malaysian Purchaser should enter “NA” in the relevant fields of the self-billed e-Invoice.

Step 3: The issuance of the self-billed e-Invoice should follow the established e-Invoice workflow.

Once the self-billed e-Invoice is validated, the Inland Revenue Board of Malaysia (IRBM) will notify the Malaysian Purchaser (no notification will be sent to the Foreign Seller).

The validated self-billed e-Invoice serves as proof of expense for the Malaysian Purchaser. There is no requirement for the Malaysian Purchaser to share this self-billed e-Invoice with the Foreign Seller.

Additionally, for self-billed e-Invoices involving imported taxable services subject to service tax as per the relevant Sales and Services Tax (SST) legislation, the taxpayer must include the service tax amount in the self-billed e-Invoice.

For the importation of goods, the Malaysian Purchaser should issue the self-billed e-Invoice by the end of the month following the month in which customs clearance is obtained.

In the case of importation of services, the self-billed e-Invoice should be issued by the end of the month following either the payment made by the Malaysian Purchaser or the receipt of the invoice from the foreign supplier, whichever occurs first. This follows the prevailing rules applicable to imported taxable services.

The required information for the self-billed e-Invoice will assist the Malaysian Purchaser in accurately issuing the self-billed e-Invoice.

Information to be Provided by the Malaysian Purchaser (Buyer) for Issuing a Self-Billed e-Invoice to the Foreign Seller (Supplier)

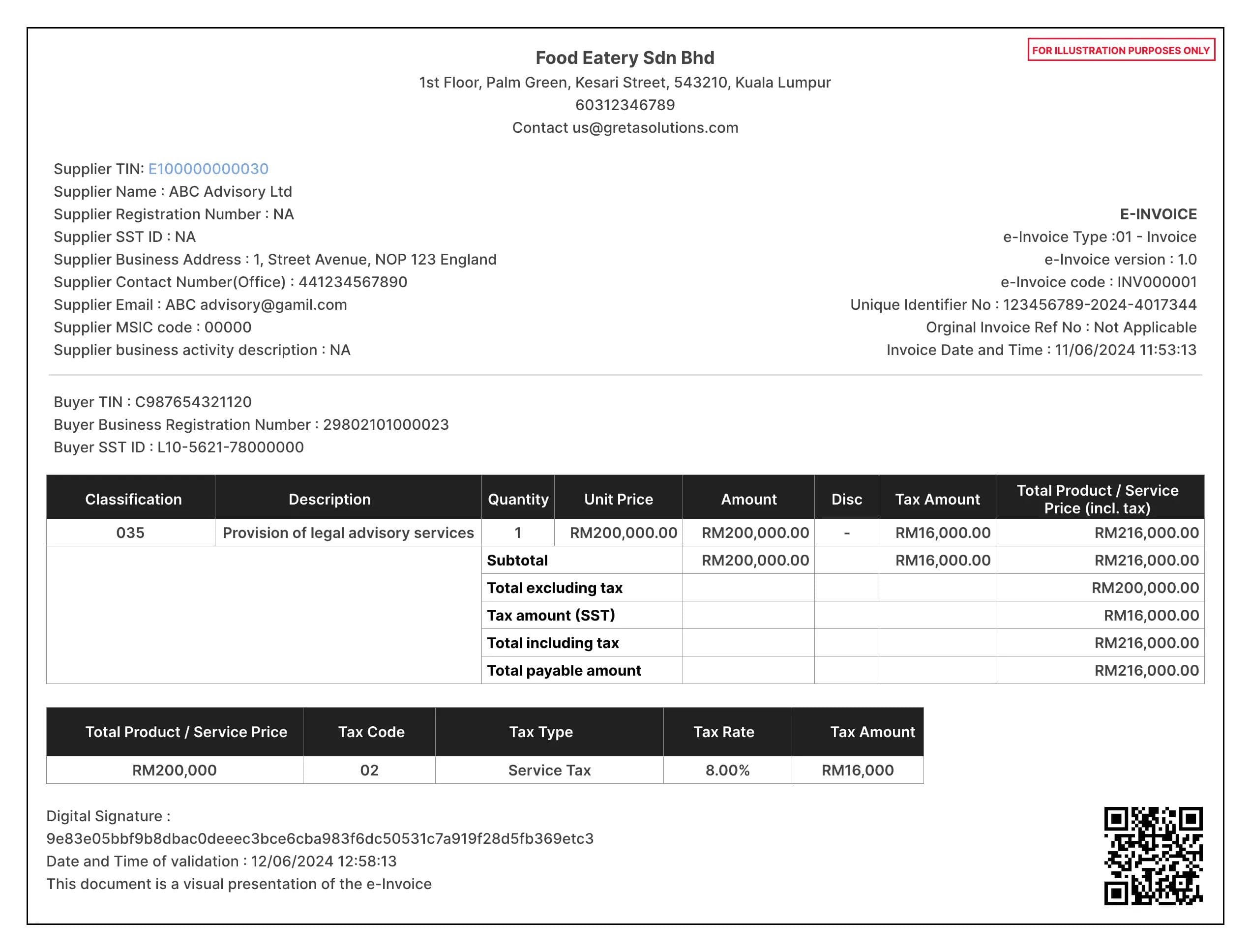

Example:

Imagine Food Eatery Sdn Bhd, a Malaysian company, has just signed an agreement with ABC Advisory Ltd, a top-notch legal advisory service provider based in the UK. Now, ABC Advisory Ltd has sent an invoice for RM200,000 for their expert legal advice concerning some issues in Malaysia. Since this advice pertains to Malaysia, it falls under the category of imported taxable services. Food Eatery Sdn Bhd made the payment on July 31, 2025.

So, what’s next? To legitimize this expense for tax purposes, Food Eatery Sdn Bhd needs to whip up a self-billed e-Invoice. Sounds fancy, right? But don’t worry, it’s not as complicated as it sounds. Basically, Food Eatery Sdn Bhd has to fill out all the necessary fields as detailed in the e-Invoice Guideline. This includes all the supplier’s details listed on the invoice. The only tricky part? The supplier’s TIN. Here, Food Eatery Sdn Bhd should input the general supplier TIN as specified in the table.

Visual example of a validated self-billed e-Invoice for a transaction with a foreign supplier in PDF format

Goods provided or services delivered by a Malaysian Seller to an International Buyer

Currently, a Malaysian seller issues an invoice, bill, or receipt to a foreign purchaser to record transactions, such as the sale of goods or the provision of services. With the implementation of e-Invoicing, the Malaysian seller is required to issue an e-Invoice to the foreign purchaser to record the income.

Steps for Issuing an E-Invoice

Step 1: Issuing the E-Invoice

Once a sale or transaction is concluded, the Malaysian seller will issue an e-Invoice to the foreign purchaser to record the transaction, whether it's for the sale of goods or the provision of services. The roles in this process are as follows:

Supplier: Malaysian Seller

Buyer: Foreign Purchaser

Step 2: Completing the Required Fields

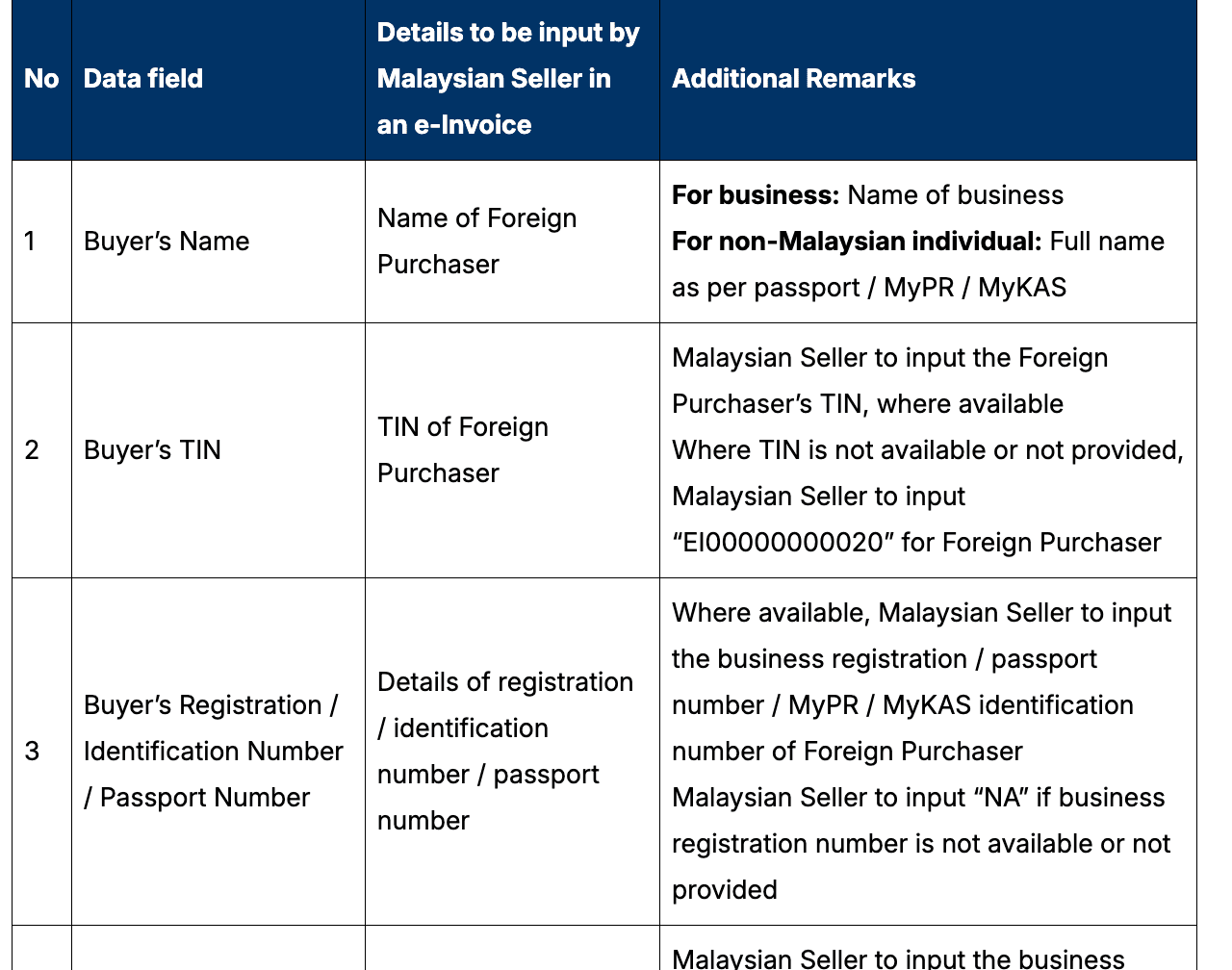

The Malaysian seller must complete the necessary fields as outlined in the e-Invoice guideline. If certain details are not available because they are not applicable to the foreign purchaser or were not provided, the seller should input "NA" in the e-Invoice.

Step 3: Following the E-Invoice Workflow

The process for issuing the e-Invoice should follow the detailed e-Invoice workflow, with some exceptions:

Once the e-Invoice is validated, the IRBM will notify the Malaysian seller only. No notification will be sent to the foreign purchaser since they are not using the MyInvois system.

The validated e-Invoice will serve as proof of income for the Malaysian seller. The seller may share a copy of the visual representation of the validated e-Invoice with the foreign purchaser for record purposes.

As the foreign purchaser is not part of the MyInvois system, there will be no request for rejection from them. If there is an error on the validated e-Invoice, any adjustment should be made by issuing a credit note, debit note, or refund note e-Invoice by the Malaysian seller.

Information Required for the E-Invoice

The information required in the e-Invoice includes all necessary data fields as outlined in the e-Invoice guideline. These details assist the Malaysian seller in issuing the e-Invoice correctly.

By adhering to these steps, Malaysian sellers can ensure compliance with the new e-Invoicing requirements, streamlining their cross-border transaction processes and maintaining accurate financial records.

Details to be provided by the Malaysian Seller (Supplier) for issuing an e-Invoice to the Foreign Purchaser (Buyer)

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.