Discover the differences between disbursements and reimbursements in Malaysia's e-invoicing system with clear examples and management steps.

Table of Contents

When dealing with Malaysia's e-invoicing system, it's crucial to understand the difference between disbursements and reimbursements. This distinction affects how expenses are recorded and managed between suppliers and buyers. Let's break down these concepts and see how they are applied through practical examples.

What Are Reimbursements?

Reimbursements refer to out-of-pocket expenses that the payee incurs while rendering services or selling goods to the payer (the buyer). These expenses are later reimbursed by the payer. Common examples include costs for airfare, travel, accommodation, telephone, and photocopying charges.

What Are Disbursements?

Disbursements, on the other hand, are expenses that the payer (the buyer) incurs but are paid to a third party by the payee. These are typically associated with services rendered or goods sold by the payee to the payer.

Current Practice in Malaysia

In Malaysia, suppliers generally include both reimbursements and disbursements in their invoices to buyers. However, this process is streamlined to ensure clarity and compliance with e-invoicing guidelines.

Key Terminologies

To simplify our discussion:

Supplier 1: The first supplier involved in the transaction.

Supplier 2: The third party or intermediary.

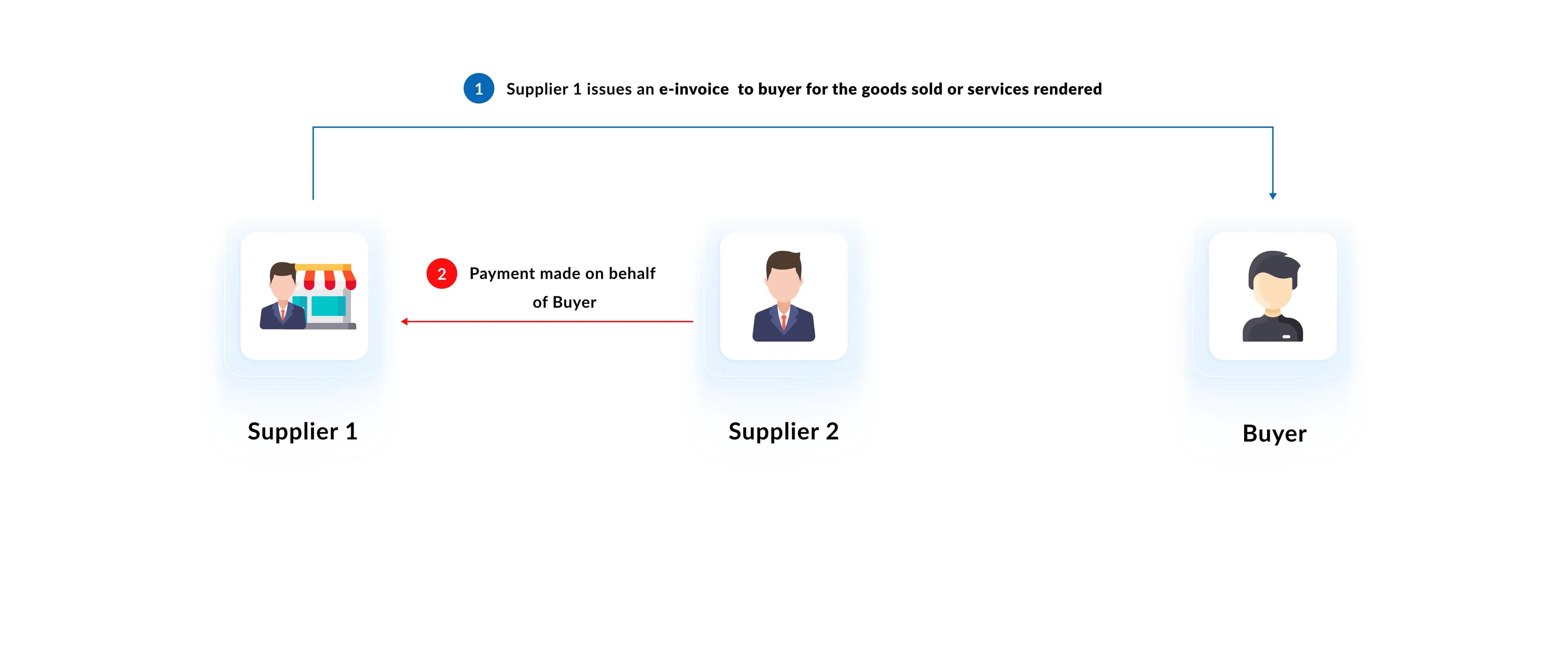

Scenario 1: Supplier 1 Issues E-Invoice to Buyer

In this scenario, Supplier 1 issues an e-invoice directly to the buyer for goods sold or services rendered. Supplier 2, acting on an agreement with the buyer, makes a payment to Supplier 1 to settle this invoice.

Steps Involved:

Agreement: Supplier 2 enters into an agreement with the buyer to supply goods or services and to make payments on behalf of the buyer.

Issuance of E-Invoice: After concluding a sale, Supplier 1 issues an e-invoice directly to the buyer as per the required fields outlined in the e-Invoice Guideline Appendices 1 and 2, and submits it to the Inland Revenue Board of Malaysia (IRBM) for validation.

Payment by Supplier 2: Supplier 2 pays Supplier 1 on behalf of the buyer and receives payment proof from Supplier 1.

Final E-Invoice by Supplier 2: Supplier 2 issues an e-invoice to the buyer for the goods or services provided, excluding the payment made on behalf of the buyer.

Example:

Perniagaan Adibah hired an event planner for a product launch on October 9, 2024. On October 1, 2024, the event planner sourced flowers from a florist, who issued an e-invoice directly to Perniagaan Adibah. The event planner then paid RM4,000 to the florist on behalf of Perniagaan Adibah on October 8, 2024, and issued an e-invoice for their services, excluding the florist's payment.

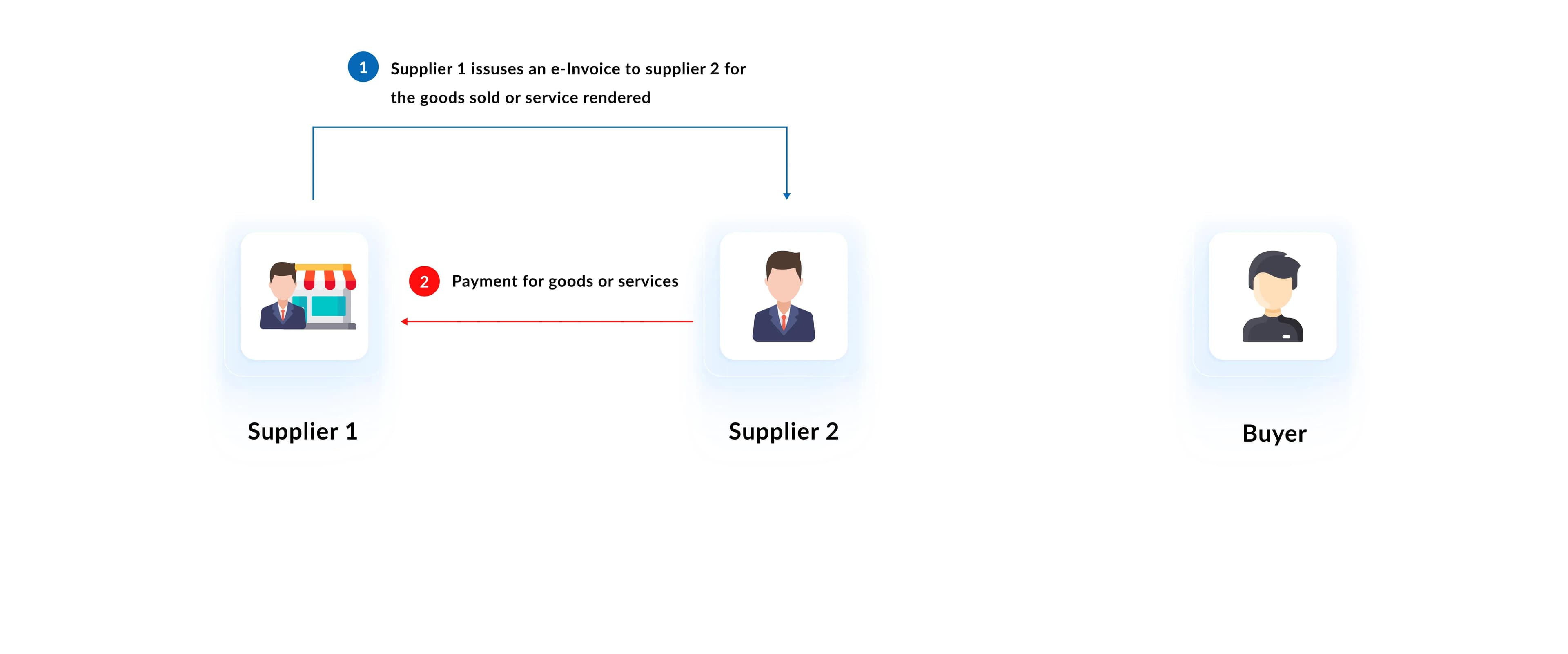

Scenario 2: Supplier 2 Issues E-Invoice to Buyer

Here, Supplier 1 issues an e-invoice to Supplier 2 for goods or services intended for the buyer. Supplier 2 then issues a separate e-invoice to the buyer, detailing the services and any disbursements or reimbursements.

Steps Involved:

Agreement: Supplier 2 agrees to supply goods or services to the buyer and handle payments on their behalf.

Issuance of E-Invoice by Supplier 1: Supplier 1 issues an e-invoice to Supplier 2 as per the required fields outlined in the e-Invoice Guideline Appendices 1 and 2, and submits it to IRBM for validation.

Payment: Supplier 2 pays Supplier 1 and receives payment proof.

Final E-Invoice by Supplier 2: Supplier 2 issues an e-invoice to the buyer, listing the service fees and disbursements as separate line items.

Example:

An event planner rented a banquet hall for Perniagaan Adibah's event, incurring RM30,000. The hotel issued an e-invoice to the event planner. The event planner then issued an e-invoice to Perniagaan Adibah, including separate line items for the service fee and the banquet hall rental.

Additional Examples

Example:

DEF Company Sdn Bhd, a subsidiary of ABC Company Sdn Bhd, received recruitment services from HR Hiring Sdn Bhd amounting to RM10,000 on September 1, 2024. HR Hiring issued an e-invoice to DEF. ABC paid HR Hiring on behalf of DEF, recording the amount owing from DEF in its books. DEF repaid ABC on December 31, 2024. No additional e-invoice was required between HR Hiring and ABC or between ABC and DEF.

In any event where ABC charges an intercompany fee to DEF for the payment made, an e-invoice is required by ABC to DEF for proof of income (for ABC) and proof of expense (for DEF).

Conclusion

Understanding the differences between disbursements and reimbursements, and how they are processed in Malaysia's e-invoicing system, is essential for compliance and clarity in financial transactions. By following the outlined steps and scenarios, businesses can ensure accurate and efficient e-invoicing practices.

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.