E-Invoicing Malaysia: Expert tips for compliant profit distribution & foreign income, including domestic & international dividends. Maximize compliance.

Table of Contents

E-Invoicing in Malaysia for Cross-Border Transactions

In Malaysia, the mandatory implementation of e-invoicing began on August 1, 2024. This new regulation requires businesses to issue e-invoices for all transactions, including cross-border transactions, where one party is located outside Malaysia. This blog will dive deep into the specifics of how businesses must generate e-invoices for international transactions, focusing on the essential steps, compliance requirements, and the necessary details.

What is E-Invoicing in Malaysia?

E-invoicing refers to the generation, transmission, and storage of invoices in a digital format, designed to streamline the invoicing process and ensure tax compliance.

In Malaysia, e-invoices must be created in structured digital formats (XML, JSON, etc.) that can be automatically processed and validated in real time by both the business and the Inland Revenue Board of Malaysia (IRBM). This helps ensure tax compliance, enhances data accuracy, and minimizes the potential for errors in financial reporting.

For cross-border transactions, the e-invoice process may vary. Typically, the seller issues an e-invoice to record the transaction. However, in certain cases—especially imports—the buyer is responsible for issuing a self-billed e-invoice.

Cross-Border Transactions: Overview and Types

According to the IRBM e-invoicing guidelines, a cross-border transaction is defined as a business activity involving at least one party in Malaysia and at least one party outside Malaysia. These transactions usually fall into two broad categories:

1. Goods/Services Sold by Foreign Sellers to Malaysian Buyers

In this case, foreign sellers issue traditional invoices or receipts based on their local practices. The Malaysian buyer is then required to issue a self-billed e-invoice to document the purchase or expense.

2. Goods/Services Sold by Malaysian Sellers to Foreign Buyers

Malaysian sellers are required to issue e-invoices for sales transactions. They are validated by the IRBM and only notified to the Malaysian seller.

Timeframes for Issuing Self-Billed E-Invoices

For imported goods and services, Malaysian buyers must adhere to specific deadlines when issuing self-billed e-invoices:

For Imported Goods:

The self-billed e-invoice must be issued by the end of the month following the month in which customs clearance is completed.

For Imported Services:

The e-invoice should be issued by the end of the month following the earlier of the two events:

Payment made by the Malaysian purchaser, or

Receipt of the invoice from the foreign supplier.

Steps to Generate E-Invoices for Cross-Border Transactions

The process for generating e-invoices depends on whether you're handling imports or exports. Below is a step-by-step guide for both scenarios:

For Imports (Self-Billed E-Invoice):

Receive the Foreign Invoice:

The foreign seller will issue a standard invoice based on their local business practices.

Generate the Self-Billed E-Invoice:

The Malaysian buyer needs to generate a self-billed e-invoice using the MyInvois System, Complyance Portal, or other API-integrated systems.

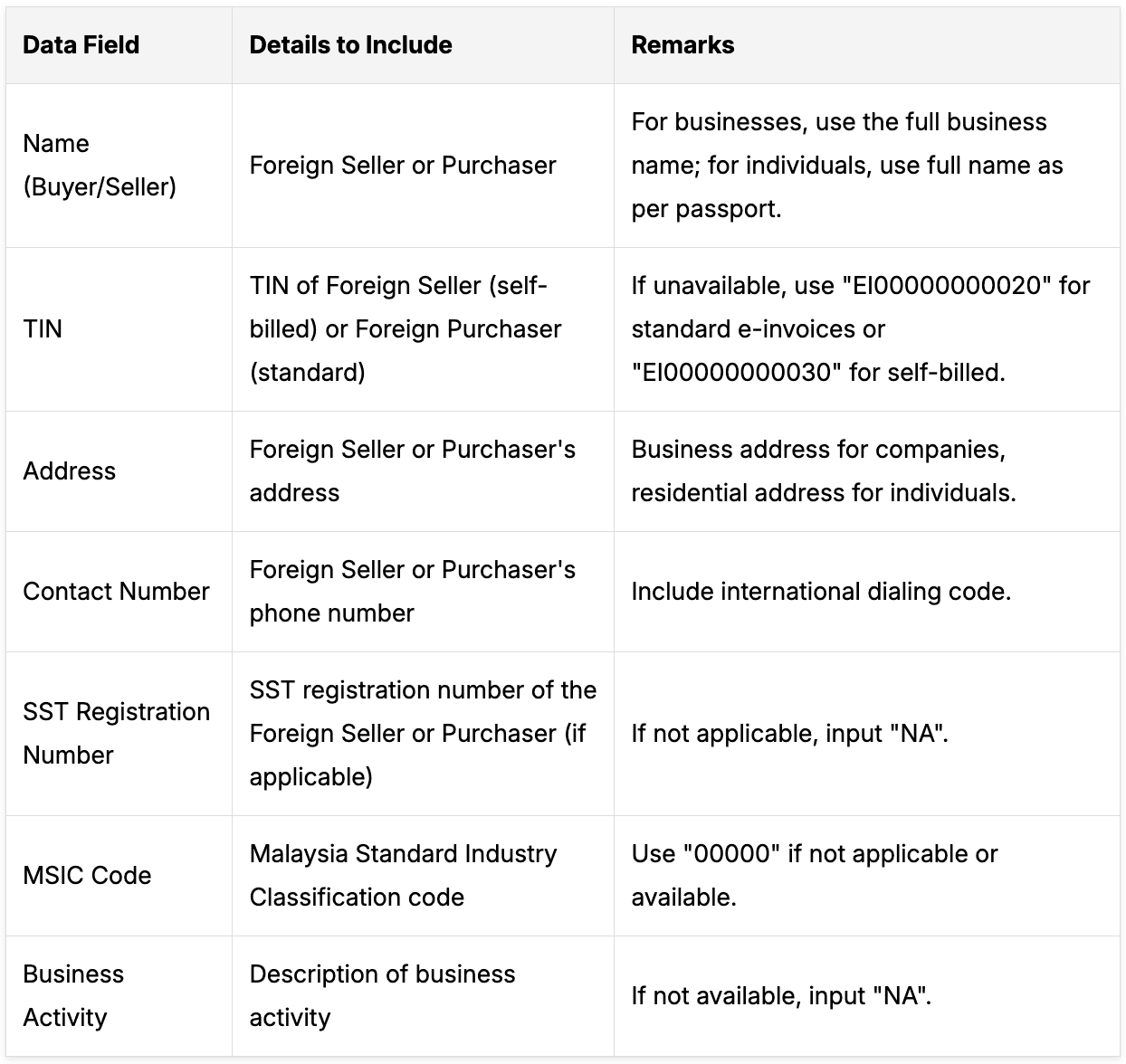

Enter Seller Details:

Input the foreign seller’s details as specified by the IRBM guidelines. This may include:

Name of the foreign seller.

TIN (Tax Identification Number)—if not available, use "EI00000000030" for self-billed invoices.

Address and other contact details.

Store the E-Invoice:

After generating the e-invoice, it must be stored for record-keeping purposes. There is no need to share it with the foreign seller.

For Exports (E-Invoice):

Issue the E-Invoice:

The Malaysian seller issues the e-invoice following the normal e-invoicing process via the MyInvois System, Complyance Portal, or API integration.

Submit Required Details:

Ensure all details are submitted accurately, following the IRBM guidelines for export-related e-invoices.

Record Keeping and Validation:

Once validated by the IRBM, the e-invoice will serve as the official proof of transaction for tax purposes.

Key Details for Generating E-Invoices in Cross-Border Transactions

The following table outlines the required details for generating self-billed e-invoices (for imports) and standard e-invoices (for exports):

Why E-Invoicing for Cross-Border Transactions is Crucial

Issuing e-invoices for cross-border transactions is essential for ensuring:

1. Tax Compliance

Malaysian businesses must comply with the SST (Sales and Service Tax) regulations. E-invoices ensure accurate tax reporting and streamline the filing process.

2. Avoiding Penalties

Failure to issue e-invoices could result in penalties of up to RM20,000, especially if the transaction is flagged during an audit.

3. Proof of Expense and Revenue

E-invoices serve as official documents for recording income or substantial expenses. This is particularly important for claiming business expenses during tax filings.

4. Smooth Customs and Payment Processing

Both the Royal Malaysian Customs Department and banks require e-invoices for customs clearance and payment processing. Without them, shipments may be delayed, or payments blocked.

Conclusion

The mandatory implementation of e-invoicing for cross-border transactions in Malaysia is designed to streamline tax compliance and simplify the invoicing process for businesses engaged in international trade.

By adhering to IRBM’s guidelines for generating self-billed and standard e-invoices, businesses can ensure smoother customs clearance, avoid penalties, and improve financial reporting

accuracy.

Ensure your business is prepared for the e-invoicing mandate and start integrating these systems to stay compliant with Malaysia's evolving tax landscape.

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.