Learn about self-billed e-invoices for payments to agents, dealers, and distributors in Malaysia, including essential methods and compliance practices.

Table of Contents

If you are running a business in Malaysia, you might not be fully aware of how e-invoicing can streamline your operations, especially when dealing with payments to agents, dealers, and distributors. These intermediaries play a crucial role in connecting your products or services with consumers and earn commissions for their efforts.

Malaysia is moving towards a digital approach in managing business transactions. E-invoicing is a key part of this shift, designed to improve transparency, reduce the chances of fraud, and ensure compliance with tax laws. By adopting e-invoicing, you can keep accurate financial records and speed up your transaction processes.

This blog aims to explain the specifics of e-invoicing in Malaysia, particularly in scenarios involving payments to agents, dealers, and distributors. We'll cover how sellers should issue e-invoices to purchasers and how sellers can create self-billed e-invoices for intermediaries. Understanding these processes will help you navigate the e-invoicing system and benefit from its advantages.

We'll also provide practical examples featuring Malaysian businesses and individuals to show how e-invoicing works in real-life situations. These examples will help clarify the roles and responsibilities of each party, making it easier for you to adopt these practices in your business.

Whether you are a business owner, an accountant, or an intermediary like an agent, dealer, or distributor, this guide is designed to help you manage e-invoicing in Malaysia effectively. Embracing e-invoicing can lead to a more efficient, transparent, and compliant business environment, fostering growth and success.

In the sections that follow, we'll walk you through the steps of issuing e-invoices and self-billed e-invoices, provide detailed scenario examples, and highlight key points to ensure you have a thorough understanding of e-invoicing in Malaysia.

General Overview

Agents, dealers, and distributors play a vital role in connecting manufacturers or service providers with consumers. These intermediaries earn commissions on each sale or service they facilitate, making them an integral part of the business ecosystem.

In Malaysia, the adoption of e-invoicing has become essential for businesses to maintain accurate records, streamline operations, and ensure compliance with regulatory requirements. The following sections will delve into the specifics of e-invoicing processes involving agents, dealers, and distributors.

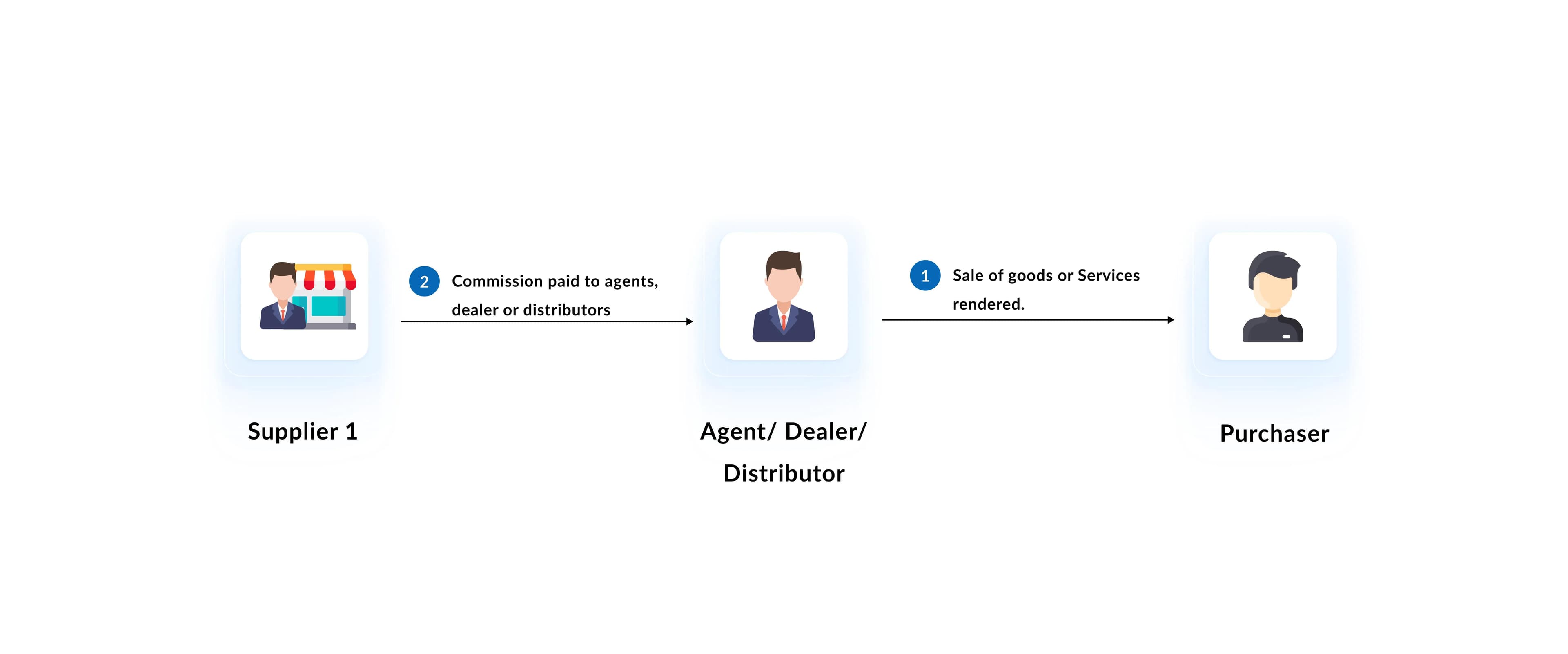

Issuance of E-Invoice from Seller to Purchaser

When a Purchaser acquires goods or services from the Seller through an Agent, Dealer, or Distributor, the Seller must issue an e-invoice to the Purchaser. This e-invoice records the transaction and serves as proof of the sale.

Roles of Parties for E-Invoice Issuance:

Supplier: Seller

Buyer: Purchaser

If the Purchaser does not request an e-invoice, the Seller will provide a normal receipt. However, the Seller must issue a consolidated e-invoice within seven (7) calendar days after the end of the month. This consolidated e-invoice aggregates all receipts issued in the previous month, serving as proof of income.

Scenario Example:Consider the scenario where Ahmad, a Malaysian retailer, purchases electronic goods from TechMart Sdn Bhd, facilitated by a dealer, Ms. Lim. Ahmad acquires a shipment of smartphones valued at RM100,000. TechMart Sdn Bhd, as the Seller, must issue an e-invoice to Ahmad to document this transaction. If Ahmad does not request an e-invoice, TechMart will issue a standard receipt instead. At the end of the month, TechMart must consolidate all such transactions and issue a comprehensive e-invoice to record the total sales.

Detailed Steps for E-Invoice Issuance:

Initiation of Transaction: The Purchaser places an order for goods or services through the Agent, Dealer, or Distributor.

Confirmation of Order: The Seller confirms the order and prepares the goods or services for delivery.

Issuance of E-Invoice: The Seller issues an e-invoice to the Purchaser, recording the details of the transaction, including the date, amount, and description of goods or services.

Delivery of Goods/Services: The Seller delivers the goods or services to the Purchaser.

Recording of Transaction: The Purchaser receives the e-invoice and records the transaction in their accounting system.

Issuance of Self-Billed E-Invoice from Seller to Agent, Dealer, or Distributor

Upon concluding a sale or transaction, the Agent, Dealer, or Distributor is eligible to receive a payment from the Seller, such as a commission. In this scenario, the Seller issues a self-billed e-invoice to the Agent, Dealer, or Distributor.

Roles of Parties for Self-Billed E-Invoice Issuance:

Supplier: Agent, Dealer, or Distributor

Buyer: Seller (assumes the role of Supplier for the purpose of issuing a self-billed e-invoice as proof of expense)

The self-billed e-invoice process is designed to ensure efficient record-keeping and compliance with Malaysian e-invoicing regulations.

Scenario Example:Imagine Sarah, a sales agent for MegaFashion Sdn Bhd, successfully sells a batch of designer clothing worth RM50,000 to various retailers. Sarah earns a 15% commission on these sales. MegaFashion Sdn Bhd, as the Seller, must issue a self-billed e-invoice to Sarah, recording the RM7,500 commission as proof of income for Sarah and proof of expense for MegaFashion. This process ensures that both Sarah and MegaFashion maintain accurate financial records.

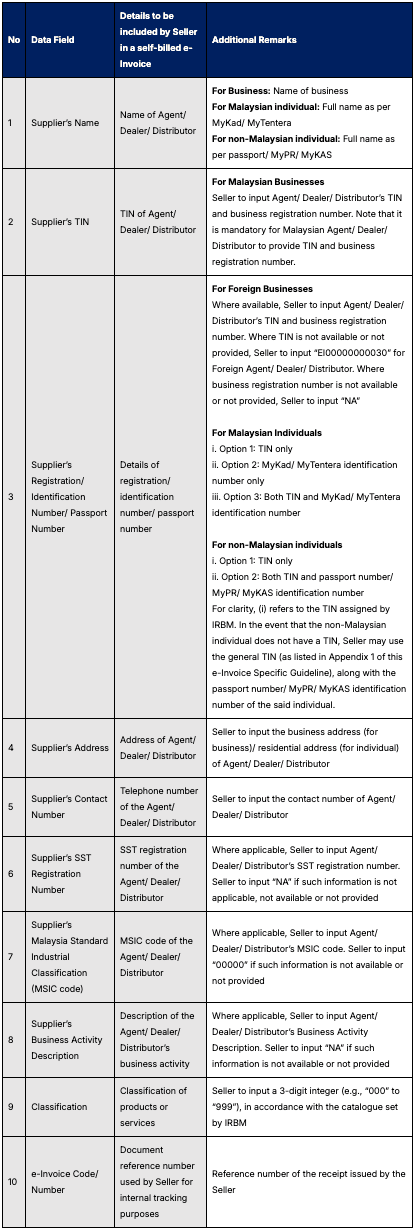

The following table provides a clear view of the data fields:

Detailed Steps for Self-Billed E-Invoice Issuance:

Completion of Sale: The Agent, Dealer, or Distributor completes the sale of goods or services to the end customer.

Calculation of Commission: The Seller calculates the commission or incentive owed to the Agent, Dealer, or Distributor based on the agreed terms.

Issuance of Self-Billed E-Invoice: The Seller issues a self-billed e-invoice to the Agent, Dealer, or Distributor, detailing the commission amount, date, and description of the transaction.

Recording of Commission: The Agent, Dealer, or Distributor records the self-billed e-invoice as proof of income, while the Seller records it as proof of expense.

Payment of Commission: The Seller pays the commission to the Agent, Dealer, or Distributor according to the agreed payment terms.

Detailed Scenario Examples

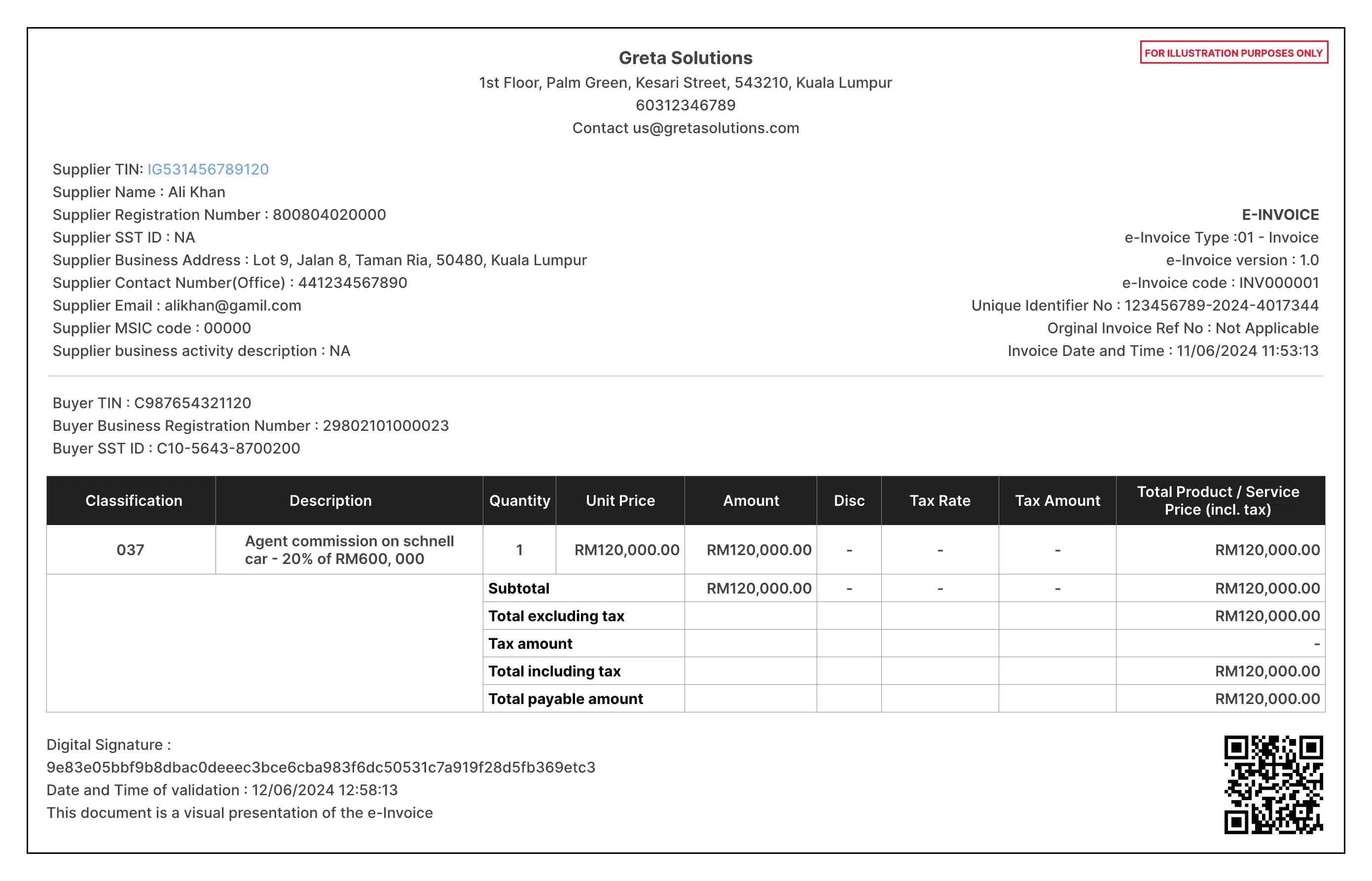

Example 1:Ali works as a sales agent for Chère Automotive Sdn Bhd (CASB). On June 22, 2024, Ali successfully sold a Schnell model car for RM600,000. As per their agreement, Ali is entitled to a 20% commission on this sale, amounting to RM120,000. CASB issues a self-billed e-invoice to Ali, recording the commission as proof of Ali’s income and CASB’s expense.

Below is an example of a self-billed e-Invoice issued by CASB to Ali:

Example 2:Rani, a distributor for HerbalCare Sdn Bhd, helps distribute health supplements to various retail stores across Malaysia. In March 2024, Rani's sales amounted to RM200,000, earning her a 10% commission of RM20,000. HerbalCare Sdn Bhd must issue a self-billed e-invoice to Rani, documenting her earnings and the company’s expenses.

Conclusion

E-invoicing in Malaysia is essential for businesses, particularly when dealing with monetary payments to agents, dealers, and distributors. This blog has provided a detailed overview of the roles of these intermediaries and the importance of issuing e-invoices and self-billed e-invoices in maintaining accurate financial records.

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.