Understand its application, benefits, and steps to issue self-billed e-invoices, including key buyer details.

Table of Contents

Understanding Self-Billed E-Invoices in Malaysia

For businesses in Malaysia, grasping the concept and application of self-billed e-invoices is essential for optimizing financial operations and ensuring tax compliance. This article explores the details of self-billed e-invoices in Malaysia and provides a thorough understanding of their use.

What is a Self-Billed E-Invoice?

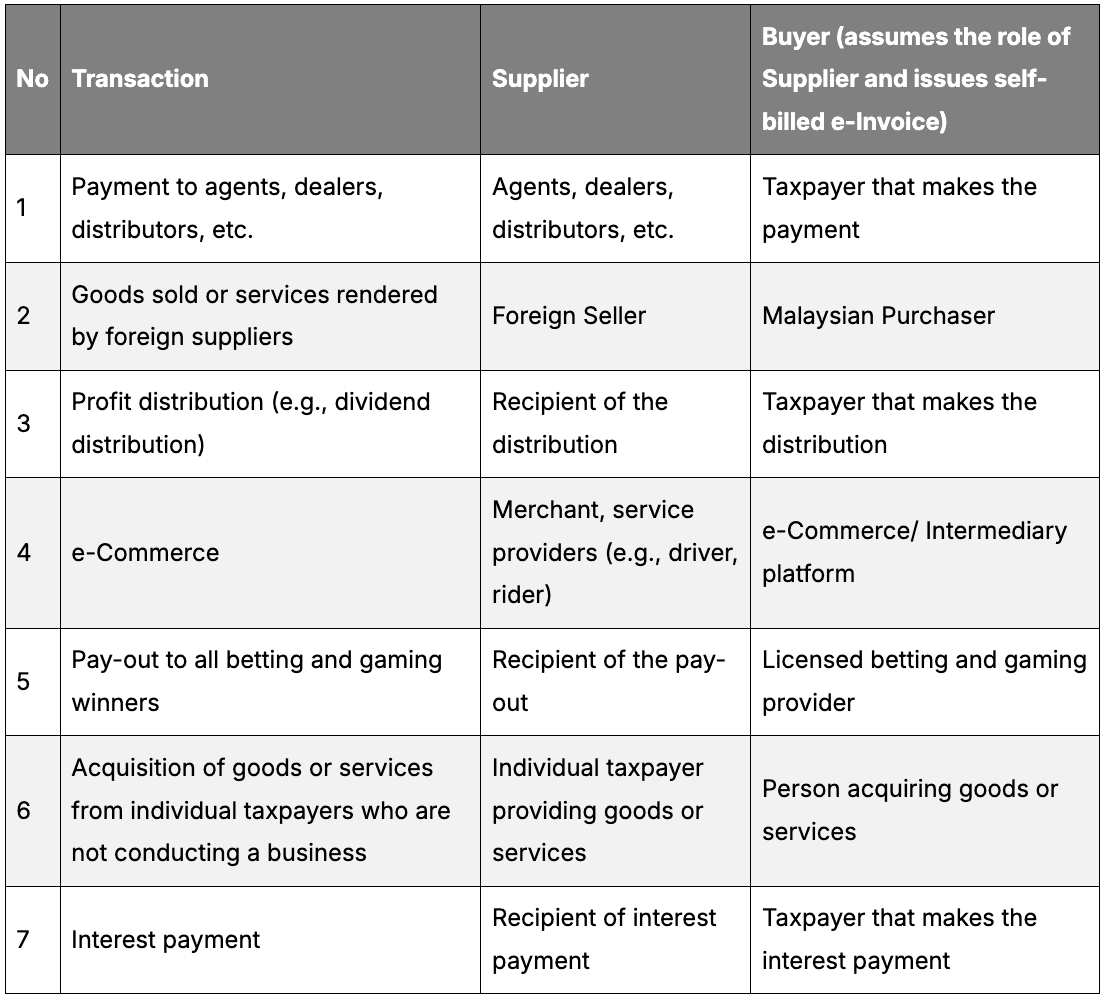

A self-billed e-invoice is a type of invoice where the buyer issues the invoice on behalf of the supplier. This process can be applied in various scenarios, such as payments to agents, dealings with foreign suppliers, profit distributions, e-commerce transactions, payouts to gambling winners, purchases from individual taxpayers, and specific interest payments.

When a buyer issues a self-billed e-invoice, they essentially assume the role of the supplier, creating an invoice to document their expenses. This facilitates precise financial records and aligns with regulatory obligations.

When Can You Use Self-Billed E-Invoices?

The guidelines outlined by the Inland Revenue Board of Malaysia (IRBM) specify certain situations where self-billed e-invoices can be used:

Payments to Agents, Dealers, and Distributors: For paying commissions or fees.

Transactions with Foreign Suppliers: When goods or services are purchased from suppliers outside Malaysia.

Profit Distribution: Such as the distribution of dividends.

E-Commerce Transactions: Involving online sales and purchases.

Payouts to Betting and Gaming Winners: For winnings paid by betting entities.

Acquisitions from Individual Taxpayers: When buying goods or services from individuals.

Specified Interest Payments: Under certain conditions specified in the guidelines.

Steps for Issuing Self-Billed E-Invoices

Input Details: The buyer inputs key details such as transaction amounts, descriptions, and applicable taxes using their ERP’s self billing .

Submit for Validation: The self-billed e-invoice is then submitted to the IRBM for validation.

Utilize the Validated Invoice: Once validated, the buyer can use the invoice as proof of expense for tax purposes.

Details Required for Self-Billed E-Invoices

In order to issue a self-billed e-invoice, the buyer must include several key details such as:

Buyer’s and supplier’s information (names, addresses, tax identification numbers)

Description of goods or services

Transaction amounts

Relevant taxes

Parties of Self-Billed E-Invoice

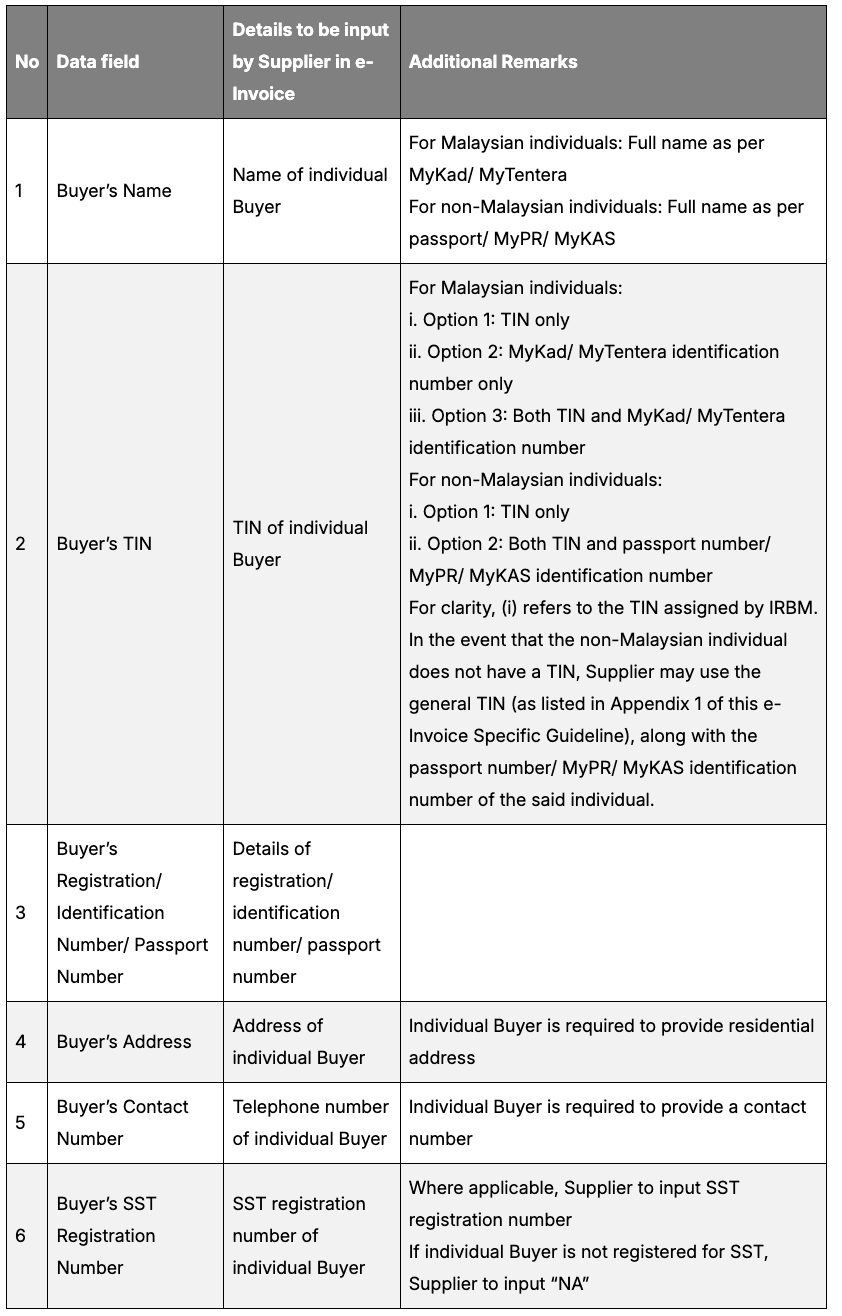

Buyer's Details for Transactions with Individuals

When issuing a self-billed e-invoice for transactions involving individual suppliers, specific details need to be recorded accurately:

Personal Information: Full name, address, and Tax Identification Number (TIN) of the individual.

Transaction Details: Detailed description of goods or services provided, transaction date, and amount.

Tax Information: Clearly indicate any applicable taxes.

Payment Method: Specify the method of payment, such as bank transfer or cheque.

Purpose of Transaction: Explicitly state the purpose of the transaction, be it for business expenses, agent commissions, etc.

Buyer’s Details for Transaction with Individuals

Ensuring these details are correctly recorded helps in meeting legal requirements and facilitates the validation process by the IRBM.

Conclusion

Ensure you take advantage of self-billed e-invoices to streamline financial transactions and foster better accountability and transparency. Understanding the roles of all parties involved and accurately documenting the buyer’s details for transactions with individual suppliers will lead to more efficient and compliant financial operations.

Familiarizing yourself with the guidelines and starting to utilize self-billed e-invoices can significantly streamline your financial processes and enhance your operational effectiveness.

The primary advantage is the ease of managing and recording transactions. It simplifies the invoicing process, ensures accurate record-keeping, aids in regulatory compliance, and reduces administrative overhead.

No, self-billed e-invoicing is only applicable under specific conditions as outlined by the Inland Revenue Board of Malaysia (IRBM) and needs IRBM approval. Ensure that your transactions qualify under the defined scenarios before proceeding with self-billing.

Key details include the buyer’s and supplier’s names and addresses, Tax Identification Numbers (TIN), a detailed description of goods or services, transaction dates, amounts, applicable taxes, payment methods, and the purpose of the transaction.

By generating and maintaining detailed records with validated invoices, self-billing aids in ensuring that all transactions are properly documented and compliant with tax regulations. The IRBM's validation process further ensures compliance.

Potential challenges include ensuring accuracy in the details submitted, understanding the eligibility criteria for transactions, and navigating the validation process with the IRBM. Proper training and system implementation can mitigate these challenges.

About the Author

Ajith Kumar

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.