Learn to issue e-invoices for profit distribution & foreign income in Malaysia. Understand guidelines for domestic & foreign dividends, staying compliant.

Table of Contents

How to Issue e-Invoices for Profit Distribution & Foreign Income?

Understanding Profit Distribution and E-Invoicing in Malaysia

Profit distribution, such as dividend payments, is a key aspect of corporate finance. In Malaysia, the process for distributing profits and related e-invoicing requirements have specific guidelines to follow. This blog will simplify these concepts and explain how e-invoicing affects both domestic and foreign profit distributions.

Domestic Profit Distribution

In Malaysia, companies distributing profits to shareholders traditionally use dividend vouchers or dividend warrants. With the introduction of e-invoicing, there are updates to these processes:

Exemptions for Certain Taxpayers: Companies listed on Bursa Malaysia and those not eligible for tax deductions under Section 108 of the Income Tax Act 1967 are exempt from issuing self-billed e-invoices for dividend distributions. This means they can continue using their existing processes, like issuing dividend vouchers or warrants.

Requirements for Other Taxpayers: Taxpayers not covered by the exemption must issue self-billed e-invoices to document the dividend distribution. The self-billed e-invoice serves as proof of income for the recipient.

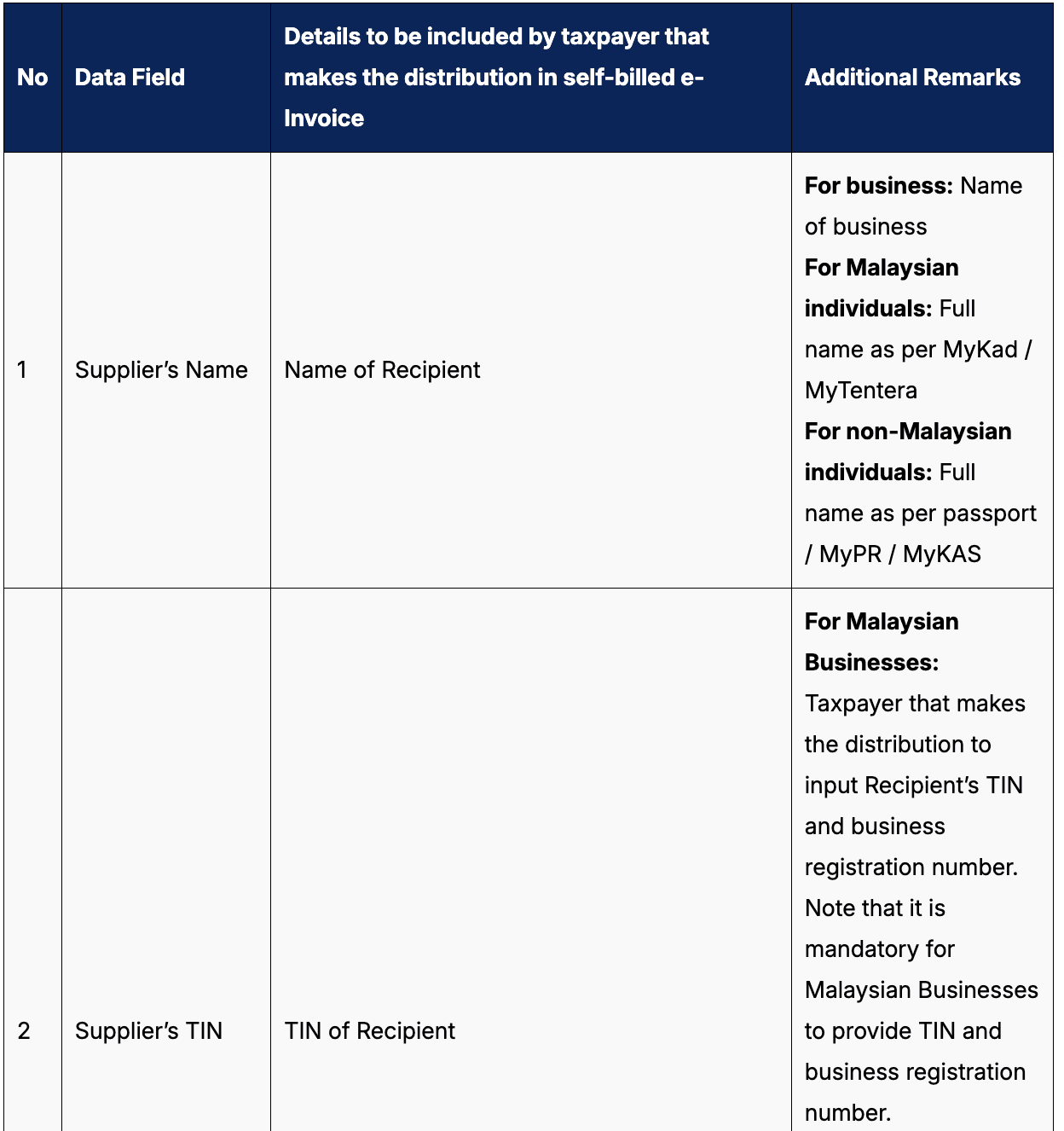

Steps for Issuing a Self-Billed E-Invoice

Issuing Dividend Voucher: When a profit, such as a dividend, is paid or credited, the taxpayer making the distribution will issue a dividend voucher to the recipient.

Self-Billed E-Invoice: The distributor must then act as the Supplier and issue a self-billed e-invoice to the recipient.

Completing the E-Invoice: Fill out the required fields in the e-invoice as specified in the e-Invoice Guideline, following the process detailed in the MyInvois Portal or via API.

Foreign Profit Distribution

For foreign profits or dividends received in Malaysia:

E-Invoice Requirement: The recipient must issue an e-invoice to document the income for tax purposes.

Roles in E-Invoicing: In this scenario, the recipient of the profit or dividend is the Supplier, and the foreign distributor is the Buyer.

E-Invoicing Process: Follow the detailed e-invoice workflow as outlined in the e-Invoice Guideline for both the MyInvois Portal and API models.

Foreign Income

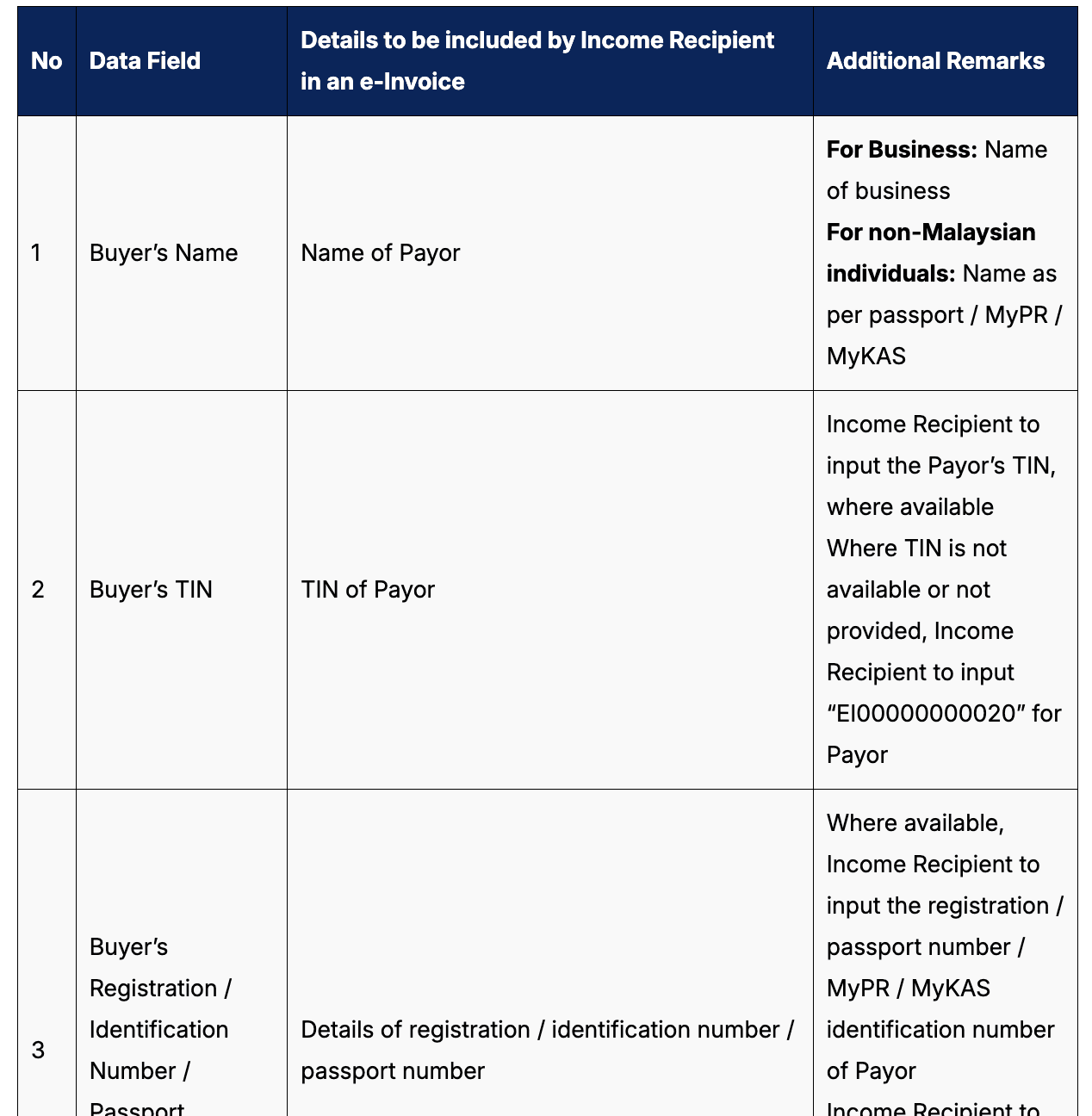

An e-Invoice is required for all foreign income received in Malaysia from outside the country as proof of income for tax purposes. Here are the steps and roles involved:

Roles for E-Invoicing:

Supplier: Recipient of the foreign income (referred to as "Income Recipient").

Buyer: Person who makes payment to the Income Recipient (referred to as "Payor").

Issuance Process:

The process of issuing an e-Invoice for foreign income is similar to the issuance of an e-Invoice involving a Malaysian Supplier and Foreign Buyer.

The Income Recipient should issue the e-Invoice by the end of the month following the month of receipt of the foreign income.

Required Information:

The information required to be included in the e-Invoice should assist the Income Recipient in issuing the e-Invoice accurately.

Conclusion

Understanding profit distribution and the associated e-invoicing requirements ensures compliance with Malaysian regulations and streamlines financial processes. Whether dealing with domestic or foreign distributions, following the correct procedures helps maintain smooth operations and proper documentation.

Im a skilled content writer and SEO expert crafting engaging articles that rank.

Passionate about making complex topics clear, discoverable, and valuable to readers.Dedicated to driving organic growth through high-quality, search-optimized content

Get the latest compliance updates, e-invoicing news, and expert tips delivered to your inbox.

ABOUT COMPLYANCE

Complyance: One API, One Platform for Global E-Invoicing

Empowering businesses to automate e-invoicing and stay compliant in 100+ countries. Our platform simplifies regulatory complexity for enterprises and fast-growing companies.

Go Live in a Week with Developer-Friendly Global E-Invoicing Platform

Complyance makes it easy for your IT/dev team to integrate once and automate E-Invoicing across 100+ countries. Built for fast deployment, field-level validation, and indirect tax accuracy—no delays, no rework.

Our Clients

We work with 500+ enterprises and brands across the globe.

Launch LHDN e-Invoicing in less than a week

Complyance solutions: your trusted partner in achieving seamless E-Invoicing integration and LHDN compliance for all ERPs in Malaysia.